基于copula-Garch 投资组合风险分析毕业论文

2021-02-24 10:28:43

摘 要

首先,本文研究背景以动态分析了四个渐进阶段,并在研究意义部分从投资角度和马科维茨的观点两个角度分析了对上述背景的的态度逐渐深入。

其次,理论部分第二章分析了时间序列边缘分布模型,第三章分析基于Copula理论的相关测度,第四章分析在险价值(VaR)。实证部分,第五章逐步研究上证指数、深证成指、中小板指三个指数之间的关系:获取基础数据后,分析数据及数据选择的原因;通过刻画样本数据时间序列图像、自相关和偏自相关图像、单位根检验对数据进行平稳性检验。通过lbq检验对样本数据进行纯随机序列检验;通过ARCH-LM检验ARCH效应;在确定存在ARCH效应后,对样本数据的t分布和正态分布进行了拟合,构建了GARCH(1,1)-t和GARCH(1,1)模型,并进行了参数估计后进行了K-S检验和Q-Q图的比较检验;然后对样本数据通过Kendall 秩相关系数及Spearman 系数分析了样本数据;结合Gumbel Copula函数、Clayton Copula 函数、Frank Copula函数,分析了样本数据的尾部相关性;最后对样本数据在以参数法和非参数法计算VaR。

最后在总结部分,针对研究期内中国金融市场的实际情况对第五章的研究结果进行具体分析。

关键词:GARCH-Copula模型,风险价值(VaR),蒙特卡洛模拟

Abstrct

First of all, the background of this paper to analyze the four progressive stages, and in the part of the study from the investment point of view and Markowitz point of view of the two perspectives on the background of the attitude of the gradual deepening.

Secondly, the second chapter analyzes the time series edge distribution model, the third chapter analyzes the correlation measure based on Copula theory, the fourth chapter analyzes the VaR. In the fifth chapter, we study the relationship between the three indexes: the data of the data and the data selection after obtaining the basic data. By depicting the time series image of the sample data, the autocorrelation And the partial autocorrelation image, the unit root test carries on the stationarity test to carry on the stationarity test. The purely random sequence test of the sample data was carried out by lbq test. The ARCH effect was examined by ARCH-LM. After determining the existence of ARCH effect, the t distribution and normal distribution of the sample data were fitted to construct GARCH (1,1) And then the sample data are analyzed by Kendall rank correlation coefficient and Spearman coefficient. The Gumbel Copula function is combined with the Gumbel Copula function, and the Gumbel Copula function is used to analyze the sample data. Clayton Copula function, Frank Copula function, the tail correlation of the sample data is analyzed. Finally, the VaR is calculated by parameter and nonparametric method

Finally, in the summary section, according to the actual situation of China's financial market during the study period, the results of the fifth chapter are analyzed in detail.

Key words: GARCH-Copula model,VaR,Monte Carlo simulation

目录

摘要 I

Abstrct II

第1章 绪论 1

1.1研究背景及意义 1

1.1.1研究背景 1

1.1.2研究意义 2

1.2国内外研究现状 2

1.2.1ARCH类模型研究现状 2

1.2.3 Copula理论的研究现状 3

1.2.4 VaR研究动态 4

1.3研究结构与论文结构安排 4

2金融时间序列的边缘分布模型 6

2.1平稳性分析 6

2.1.1平稳时间序列的基本框架 6

2.1.2平稳性检验 6

2.2纯随机性分析 8

2.2.1纯随机序列的定义与性质 8

2.2.2纯随机检验 8

2.3 ARCH效应分析 9

2.3.1ARCH效应定义与性质 9

2.3.2 ARCH效应检验 9

2.4 ARCH类模型 9

2.4.1线性ARCH模型 9

2.4.2 GARCH模型 10

2.4.3 EGARCH模型 11

2.5ARCH模型检验 12

3 Copula理论与相关性分析 12

3.1 Copula函数的定义 13

3.2copula函数的分类 13

3.2.1阿基米德copula函数 14

3.2.2二元阿基米德copula函数 14

3.2.3常用的阿基米德copula函数 14

3.3copula函数的相关性测度 15

3.3.1copula函数相关性测度的特点 15

3.3.2Kendall 秩相关系数τ 15

3.3.3 Spearman相关系数ρ 16

3.4基于copula函数的尾部相关测度 16

3.4.1尾部相关系数 17

4在险价值VaR 17

4.1 VaR的定义 18

4.2 VaR的计算 18

4.2.1参数法 18

4.2.2非参数法中的蒙特卡洛模拟 19

5基于模型的投资组合风险的实证分析 20

5.1样本数据选择及简单统计描述 21

5.1.1样本数据选择 21

5.1.2样本数据的基本统计特征 21

5.2平稳性检验 23

5.2.1图像检验 23

5.2.2 ADF检验 25

5.3 lbq检验 26

5.4 ARCH-LM检验 26

5.5 GARCH模型的构建与比较 27

5.5.1 GARCH模型的构建 28

5.5.2模型的比较检验 29

5.6样本收益率数据的相关性及尾部相关 31

5.6.1相关性分析 31

5.6.2尾部相关性分析 32

5.6.3市场风险估计 33

6总结与展望 34

6.1总结 35

6.2展望 36

参考文献 36

致谢 39

附录 40

第1章 绪论

1.1研究背景及意义

1.1.1研究背景

从全球市场这一最大的宏观视角来看,经济全球化和金融一体化趋势的纵深发展。而就金融行业内部而言,金融创新与技术进步使得行业内部整体实力不断加强。在内外相互作用之下,金融市场内部发生了基础性、结构性的变化。而这种变化是渐变的,因此本文的研究背景采用动态分阶段的分析方法。

第一阶段,就整体而言,在一个符合行业发展需要并不断强化的趋势之下,原有整体内部的各个子系统联系不断加强,使得原有整体变成一个内部结构流动性强的深层次有机体。具体而言,金融市场的全球化特征不断加强,金融全球化趋势势在必行。金融全球化是指在各国家地区之间的交流合作程度日渐加深,在此基础之上相互渗透影响,最终国家、地区等明确的地域界限模糊,因而各国间金融活动迅速溢出本国界限,向外流动,最终全球金融形成整体。

第二阶段,在整体构架初步形成之后,各个子系统之间的联系得到进一步加强,使得内部构架更具连通性、开放性:作为整体构成的各国资本以数量大、速度快、流动方向有序的特点在整体运行空间内进一步流动。各国资本具有不同的风险特质在以不同方式组合配置之后,结果表现为:横向上,使得金融市场具有相异的内部运行方式及外部表现形式;纵向上,在时间的不断累积及程度不断加深之下其在量与质双向上都会有所提高,即金融市场内部的交易种类日趋多元化,即不仅包含国内大型企业如国企、央企的大盘股,也会形成有中小企业够成的中小板指数、创业板指数等,由此投资者拥有了更多的投资选择以适应投资者不同的风险承受能力。并且相关性弱的股票构成投资组合可以稀释了市场的非系统性风险,投资门槛进一步降低,由此交易量增加。这种“同结构,强联系”的发展模式势必会使金融市场内部联动性增强:各子系统的价格协调作用可以再短时间内,以局部为起点迅速向周围扩散蔓延,这样整体就形成了“牵一发而动全身”之势。

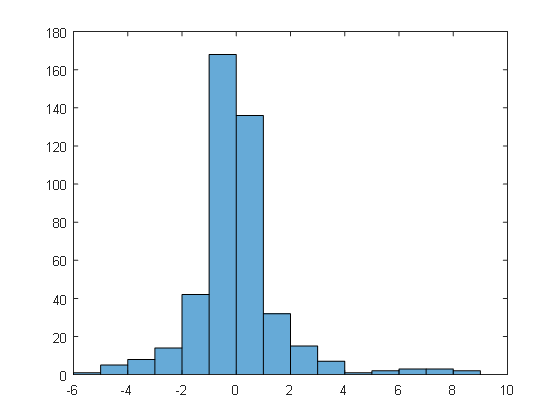

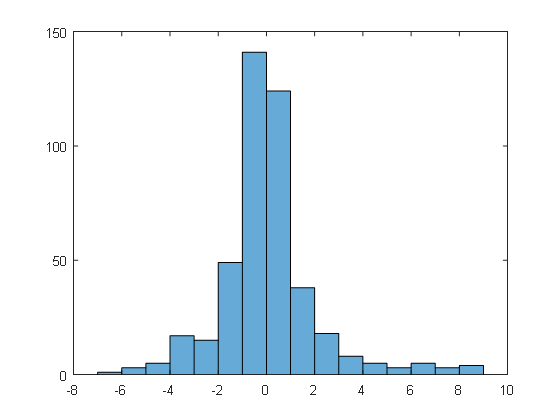

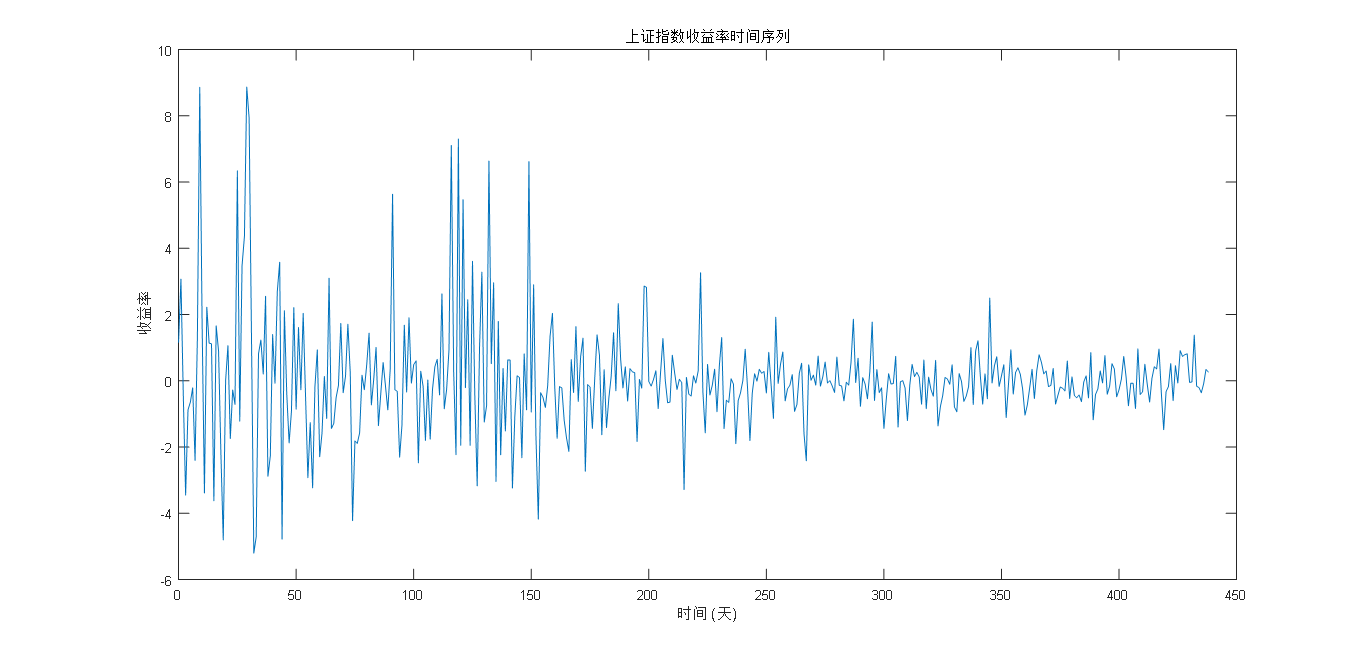

相关图片展示: